From a 20-Year Lending Insider

Stop Answering. Start Strategizing.

The collector on the other end of that phone has a strategy. They know what they paid for your debt. They know their profit margins. They know exactly how low they can go. You deserve to know the same.

Who's Really Calling You?

Before you pick up the phone, send a letter, or pay a dime you need to know who you're dealing with.

The wrong strategy with the wrong collector costs you money.

⚠️ Debt Buyer

OWNS your debt outright

Paid pennies on the dollar (5-10 cents)

Profit model: Anything above cost = profit

Controls credit reporting (can delete)

Will negotiate aggressively

More likely to sue for larger amounts

📋 Collection Agency

Does NOT own your debt

Works on commission (25-50%)

Original creditor sets the terms

Cannot delete creditor controls reporting

Less flexibility to negotiate

May return debt to creditor if unpaid

Lender's Truth: Debt buyers have flexibility because they profit regardless of settlement amount. Collection agencies

answer to the original creditor which limits what they can offer you.

🎯 The Collector's Playbook

Call Early, Call Often

Multiple calls per day, different numbers, pressure tactics. They're testing your breaking point.

Create Urgency & Fear

"Pay today or we'll sue." "This is your final notice." Most threats are empty they want panic payments.

Offer "Discounts" That Aren't

"We'll settle for 70%!" They paid 5 cents on the dollar. That 70% is still massive profit.

Count on Your Ignorance

They know most people don't understand validation rights, SOL, or negotiation math.

Your Counter-Strategy

Know who owns your debt. Understand the math. Negotiate from knowledge not desperation.

They Paid $50 for Your $1,000 Debt

$1,000

Your Original Debt

$50

What They Paid

$200

Your Settlement

💡 If you settle at 20% ($200), they STILL profit $150. The math is in YOUR favor—you just need to know how to use it.

Pay? Settle? Ignore? Dispute?

The answer depends on YOUR situation. This bundle teaches you how to decide:

💰 Pay

When it's recent, small, and you can get pay-to-delete in writing

🤝 Settle

When it's a debt buyer, you have leverage, and you know the math

⏳ Wait

When SOL is near, they can't prove ownership, or timing matters

📝 Dispute

When there are errors, duplicate reporting, or inaccurate info

⚠️ The wrong move at the wrong time can restart the clock or trigger a lawsuit. Strategy matters.

What's Inside Collection Truth 365

The Breakdown

What collections are (and aren't)

Charge-off vs collection difference

How debt moves through the system

Who owns your debt

Common myths debunked

FICO score impact breakdown

The Strategy

6 letter types explained

Validation vs dispute letters

Critical timing windows

When NOT to send letters

Pay-to-delete negotiation

Decision trees for every scenario

The Rebuild

Credit union advantages

Utilization strategy (30% vs 10%)

Two-payment trick for fast gains

What NOT to do (subprime traps)

Your 6-month roadmap

FICO vs VantageScore truth

Bonuses Included

Debt Buyer vs Agency Guide

Top 10 collectors + settlement ranges

State-by-State SOL Guide

Negotiation scripts

When to offer what percentage

Pay-to-delete request templates

Hey, I'm Lisa and I know exactly what lenders look for..

I spent 20 years in lending. I sat at the underwriter's desk. I reviewed thousands of credit reports. I know exactly what stops approvals and what gets you through manual underwriting.

But here's the thing: I also saw good people denied for the wrong reasons. I saw myths destroy credit. I saw people follow templates that made things worse.

That's why I don't sell credit repair. I teach you how to rebuild from a lender's perspective the real strategy that actually works.

I've helped 500+ people go from confused to confident. Now it's your turn.

20+ years in credit union lending (personal, auto, mortgage, HELOC)

12 years as lending & collections supervisor

Specialized in subprime and risk-based lending

Board Certified Credit Consultant (NACCC)

STILL NOT SURE?

Frequently Asked Questions

What format are these?

All guides are delivered as downloadable PDFs. You'll get instant access after purchase no waiting, no shipping.

Is this the same as credit repair?

No. This teaches you STRATEGY how to negotiate with collectors, when to pay vs settle vs dispute, and how lenders actually evaluate your credit. No magic letters. Real knowledge.

Do I need Charge-Off 365 too?

They're different products. Collection Truth 365 focuses on dealing with collectors and negotiation. Charge-Off 365 focuses on charge-off impact and rebuilding. If you have both issues, both bundles help.

Will this work for old collections?

Yes, the strategy changes based on age. You'll learn about statute of limitations, when older debts are "zombie debt," and how to handle collections at every stage.

What if I need more help?

You can add a personalized Credit Audit ($97) where I review YOUR specific credit file and give you a custom action plan with a Loom video walkthrough.

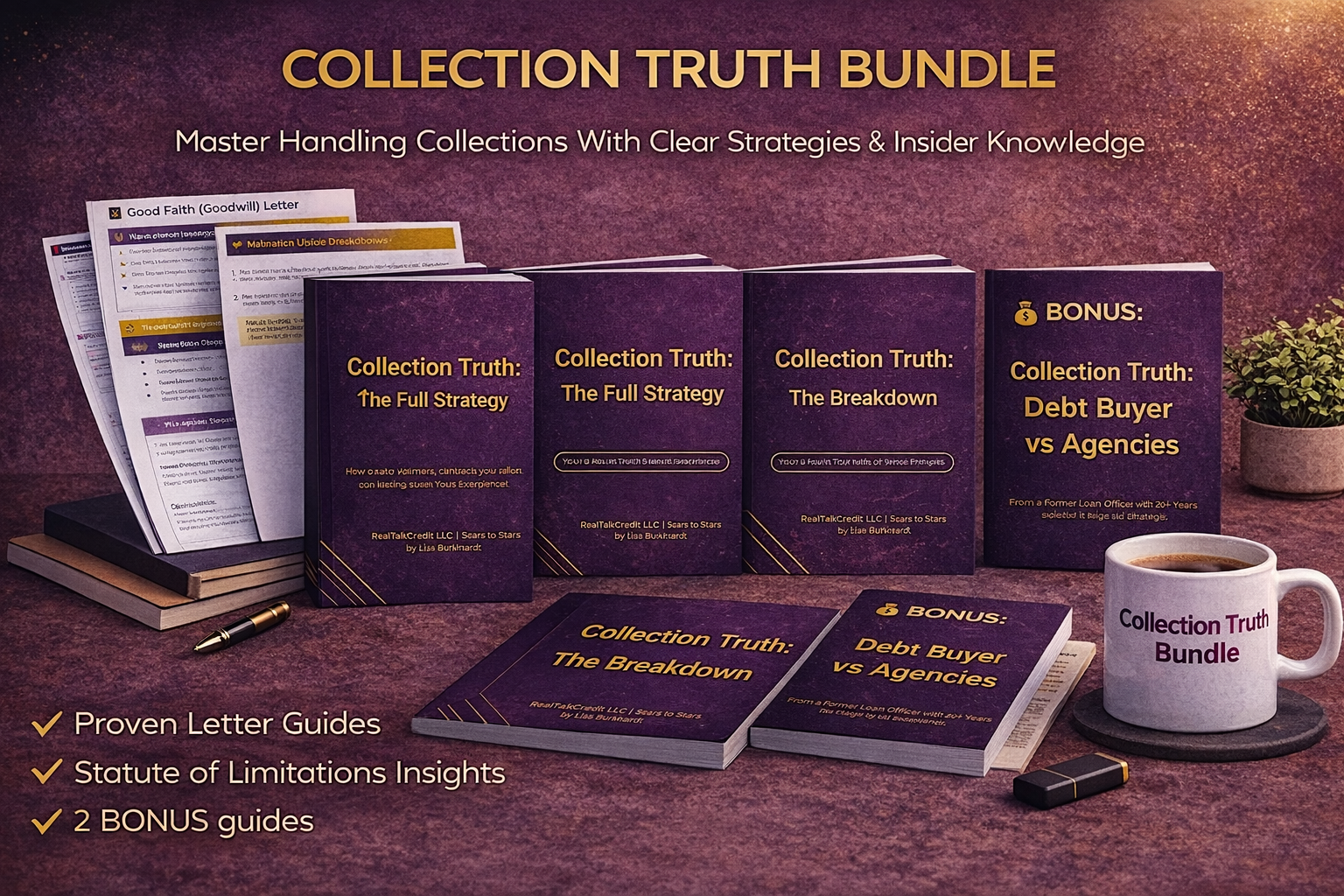

Complete bundle

Collection Truth Bundle

Instant Download

Get the Full System

Part 1: The Breakdown

Part 2: The Full Strategy

Part 3: The Rebuild

Debt Buyer vs Agencies Guide

State-by-State SOL Guide

Total value: $205

Today Just $97

Copyrights 2025 | RealTalk Credit LLC | All Rights Reserved | Terms & Conditions | Privacy Policy | Legal Disclaimer

Disclaimer for site: This is not credit repair or legal advice. All tools and coaching provided are for educational purposes only.